Chapter 8 - Volatility Spreads

第八章 - 波动率价差

To take advantage of a theoretically mispriced option, it is necessary to hedge the purchase or sale of the option by simultaneously taking an opposing market position. In the examples in Chapter 5, the opposing market position was always taken in the underlying instrument. It is also possible to hedge an option position with other options which are theoretically equivalent to the underlying instrument. For example, suppose we feel a certain call with a delta of 50 is underpriced in the marketplace. If we buy 10 calls, giving us a total delta position of +500, we can hedge our position in any of the following ways:

- Sell five underlying contracts

- Buy puts with a total delta of -500

- Sell calls, different than those which we purchased, with a total delta of +500

- Combine several of these strategies, such that we create a total delta of -500

为了利用理论上被错误定价的期权,需在买入或卖出期权的同时采取相反的市场头寸进行对冲。在第五章的示例中,对冲头寸总是建立在标的资产上。不过,也可以用其他与标的资产理论上等同的期权来对冲。例如,假设我们认为某个delta值为50的看涨期权价格过低。如果我们买入10份看涨期权,总delta头寸为+500,可以用以下几种方式对冲:

- 卖出5份标的合约

- 买入delta总值为-500的看跌期权

- 卖出不同于买入的看涨期权,总delta为+500

- 组合多种策略,形成总delta为-500

With many different calls and puts available, as well as the underlying contract, there are many different ways of hedging our ten calls. Regardless of which method we choose, each spread will have certain features in common:

- Each spread will be approximately delta neutral.

- Each spread will be sensitive to changes in the price of the underlying instrument.

- Each spread will be sensitive to changes in implied volatility.

- Each spread will be sensitive to the passage of time.

由于有多种看涨和看跌期权可用,再加上标的合约,我们有许多方法对这10份看涨期权进行对冲。不论选择哪种方法,每种价差策略都会具备以下特点:

- 每种价差策略都近似为delta中性。

- 每种价差策略都对标的资产价格变化敏感。

- 每种价差策略都对隐含波动率变化敏感。

- 每种价差策略都会受时间推移影响。

Spreads with the foregoing characteristics fall under the general heading of volatility spreads. In this chapter we will define the basic types of volatility spreads and look at their characteristics, initially by examining the expiration values of the spread, and then by considering the delta, gamma, theta, vega, and rho associated with each spread.

具备上述特征的价差策略一般称为波动率价差。本章将定义波动率价差的基本类型,并通过分析价差的到期价值、delta、gamma、theta、vega和rho等因素来探讨其特性。

Before defining the primary types of spreads, it should be noted that spreading terminology is not uniform. Traders sometimes use different terms when referring to the same spread; they sometimes use the same term when referring to different spreads. An attempt has been made to use the most common terminology, but alternative spread definitions are also given where appropriate.

在定义主要的价差类型前需注意,价差的术语并不统一。交易者有时会用不同术语指代同一种价差,有时会用相同术语指代不同的价差。我们尽量使用最通用的术语,但在适当的情况下也会提供其他定义。

BACKSPREAD

反向价差

(also referred to as a ratio backspread or long ratio spread)

(也称为比率反向价差或多头比率价差)

A backspread is a delta neutral spread which consists of more long (purchased) options than short (sold) options where all options expire at the same time. In order to achieve this, options with smaller deltas must be purchased and options with larger deltas must be sold. A call backspread consists of long calls at a higher exercise price and short calls at a lower exercise price. A put backspread consists of long puts at a lower exercise price and short puts at a higher exercise price.

反向价差是一种delta中性策略,由更多买入的期权和更少卖出的期权组成,所有期权的到期日相同。要实现该策略,需买入delta较小的期权,卖出delta较大的期权。看涨反向价差通常是以较高的行权价买入看涨期权、较低的行权价卖出看涨期权;看跌反向价差则是以较低的行权价买入看跌期权、较高的行权价卖出看跌期权。

Typical backspreads and their values at expiration are shown in Figures 8-1 and 8-2. (These, and the example spreads in the following sections, are taken from the option evaluation table in Figure 8-20.) In each case, a move away from the long option's exercise price will increase the value of the spread. Depending on the type of backspread, movement in one direction may be preferable to movement in the other direction. In a call backspread the upside profit potential is unlimited; in a put backspread the downside profit is unlimited. But the primary consideration is that some movement will occur. If no movement occurs, a backspread is likely to be a losing strategy.

图8-1和图8-2展示了典型的反向价差及其到期时的价值。(这些示例及后续部分的价差取自图8-20的期权评估表。)在每种情况中,标的价格远离买入期权的行权价时,价差价值会增加。具体而言,看涨反向价差在上涨中潜在利润无限;看跌反向价差在下跌中利润无限。但关键是价格需要发生明显的波动,若无波动,反向价差策略可能会亏损。

图8-1中:

long 30 March 105 calls (24)

short 10 March 95 calls (78)

long 30 March 105 calls (24)

short 10 March 95 calls (78)

括号里的数字是delta值。long的delta小于short的delta。买入合约数量多余卖出数量。

图8-2中一样,只不过long的delta绝对值小于short的delta绝对值。

Typically, a backspread is done for a credit. That is, the amount of premium received for the sold options is greater than the premium paid for the purchased options. This ensures that the backspread will be profitable if the market makes a large move in either direction. If the market collapses in the case of a call backspread, or the market explodes in the case of a put backspread, all options will expire worthless and the trader will keep the credit from the initial transaction.

通常,反向价差是以净收入(credit)方式建立的,即卖出期权所获权利金高于买入期权支付的权利金,这确保了在市场大幅波动时策略能盈利。如果看涨反向价差中市场崩溃,或在看跌反向价差中市场剧烈上涨,所有期权均将归零,交易者可保留初始交易的净收入。

A trader will tend to choose the type of backspread which reflects his opinion about market direction. If he foresees a market with great upside potential, he will tend to choose a call backspread; if he foresees a market with great downside potential he will tend to choose a put backspread. He will avoid backspreads in quiet markets since the underlying contract is unlikely to move very far in either direction.

交易者会根据对市场走势的预期选择合适的反向价差类型。如果预期市场有较大上涨空间,倾向于选择看涨反向价差;若预期市场有较大下跌空间,则倾向于选择看跌反向价差。在市场平静、标的合约波动不大时,交易者通常会避免使用反向价差策略。

RATIO VERTICAL SPREAD

比率垂直价差

(also referred to as a ratio spread, short ratio spread, vertical spread, or front spread)

(也称为比率价差、空头比率价差、垂直价差或正向价差)

A trader who takes the opposite side of a backspread also has a delta neutral spread, but he is short more contracts than long, with all options expiring at the same time. Such a spread is sometimes referred to as a ratio spread or a vertical spread. However, these terms can also be applied to other types of spreads. In order to avoid later confusion, we will designate the opposite of a backspread as a ratio vertical spread.

采取与反向价差策略相对立场的交易者也可以建立一个delta中性价差,但其空头合约数量多于多头合约,且所有期权的到期日相同。此类价差有时称为比率价差或垂直价差,不过这些术语也适用于其他类型的价差。为了避免混淆,我们将反向价差的对立面称为“比率垂直价差”。

Typical ratio vertical spreads, and their expiration values, are shown in Figures 8-3 and 8-4. From these graphs we can see that a ratio vertical spread will realize its maximum profit at expiration when the underlying contract finishes right at the short (sold) option's exercise price. Since a ratio vertical spreader assumes the opposite risks of a backspreader, his risk is unlimited on the upside in a call ratio vertical spread, and unlimited on the downside in a put ratio vertical spread. While a ratio vertical spreader expects the market to remain relatively stable, he will tend to choose either a call or put ratio vertical spread in order to limit his losses if he is wrong. If he is primarily worried about a swift rise in the market, he will choose a put ratio vertical spread; if he is primarily worried about a swift fall in the market, he will choose a call ratio vertical spread. In both cases, if the market does make a big move, his loss will be limited since the calls can only collapse to zero if the market falls, and the puts can only collapse to zero if the market rises.

典型的比率垂直价差及其到期价值如图8-3和图8-4所示。从这些图表中可以看出,比率垂直价差在标的合约价格恰好收于卖出期权的行权价时实现最大利润。由于比率垂直价差承受着与反向价差相反的风险,看涨比率垂直价差在价格上升时风险无限,而看跌比率垂直价差在价格下跌时风险无限。比率垂直价差交易者通常预期市场保持相对稳定,但会选择看涨或看跌比率垂直价差来限制错误时的损失。如果主要担心市场快速上涨,则选择看跌比率垂直价差;如果担心市场快速下跌,则选择看涨比率垂直价差。在这两种情况下,如果市场发生大幅波动,其损失会被限制,因为市场下跌时看涨期权最多归零,而市场上涨时看跌期权最多归零。

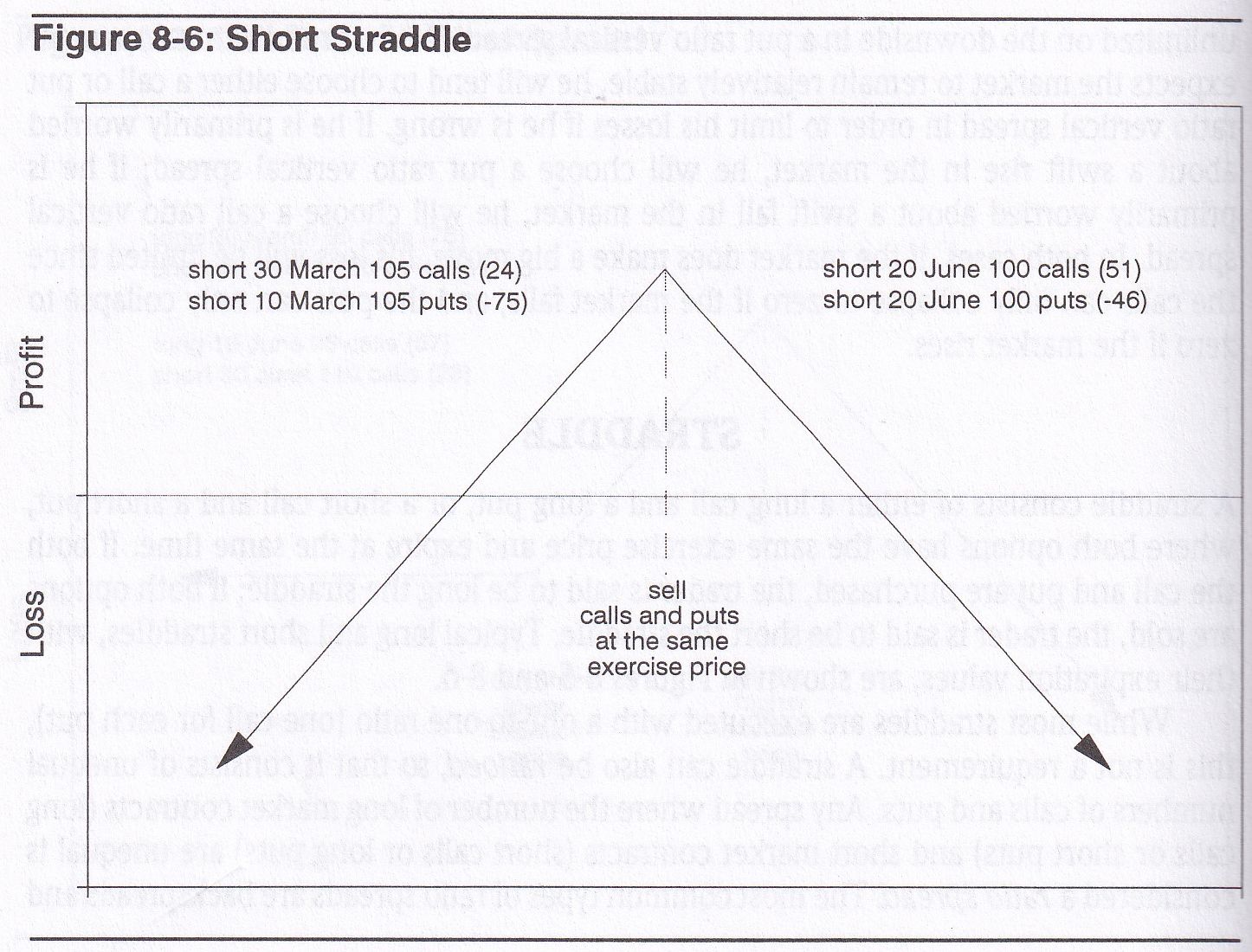

STRADDLE

跨式期权

A straddle consists of either a long call and a long put, or a short call and a short put, where both options have the same exercise price and expire at the same time. If both the call and put are purchased, the trader is said to be long the straddle; if both options are sold, the trader is said to be short the straddle. Typical long and short straddles, with their expiration values, are shown in Figures 8-5 and 8-6.

跨式期权由一个买入看涨期权和一个买入看跌期权,或一个卖出看涨期权和一个卖出看跌期权组成,两个期权行权价格相同,到期日一致。买入跨式期权称为做多跨式期权,卖出跨式期权称为做空跨式期权。典型的做多和做空跨式期权及其到期价值如图8-5和图8-6所示。

While most straddles are executed with a one-to-one ratio (one call for each put), this is not a requirement. A straddle can also be ratioed, so that it consists of unequal numbers of calls and puts. Any spread where the number of long market contracts (long calls or short puts) and short market contracts (short calls or long puts) are unequal is considered a ratio spread. The most common types of ratio spreads are backspreads and ratio vertical spreads. But other spreads, including straddles, can be ratioed. This is usually done to ensure that the spread is delta neutral.

尽管大多数跨式期权按一比一比例执行(一份看涨期权对应一份看跌期权),但这并非硬性要求。跨式期权也可以设置成不同比例,即由不等数量的看涨和看跌期权组成。只要多头和空头市场合约(如多头看涨或空头看跌和空头看涨或多头看跌)数量不相等,就属于比率价差。常见的比率价差包括反向价差和比率垂直价差,但其他价差形式,包括跨式期权,也可以设置成比率化,通常是为了实现delta中性。

A long straddle has many of the same characteristics as a backspread. Like a backspread it has limited risk and unlimited profit potential. With a long straddle, however, the trader's potential profit is unlimited in either direction. If the market moves sharply up or down, the straddle will realize ever increasing profits as long as the market continues to move in the same direction.

做多跨式期权与反向价差有许多相似之处,二者都具有有限风险和无限利润潜力。不同的是,做多跨式期权的潜在利润在市场剧烈上升或下降时均可获得。如果市场大幅波动,跨式期权会随着市场持续波动方向而不断增加收益。

A short straddle has many of the same characteristics as a ratio vertical spread. The spread will realize its maximum profit if the market stays close to the call and put exercise price. The spread has a limited profit potential, and unlimited risk should the market move violently in either direction.

做空跨式期权则与比率垂直价差特征相似。当市场价格接近看涨和看跌期权的行权价时,价差可获得最大利润。此价差的利润潜力有限,但市场若向任一方向剧烈波动则风险无限。

The new option trader often finds long straddles attractive because strategies with limited risk and unlimited profit potential offer great appeal, especially when the profit is unlimited in both directions. However, if the hoped for movement fails to materialize, he soon finds that losing money little by little, even a limited amount, can also be a painful experience. This is not an endorsement of either long or short straddles. Under the right conditions either strategy may be sensible. But the intelligent trader's primary concern ought to be the total expected return. If the strategy with the greatest expected return also entails unlimited risk, a trader may have to accept that risk as part of doing business.

许多新手交易者对做多跨式期权策略情有独钟,因为它风险有限但利润无限,尤其是上下行皆有盈利潜力。然而,如果市场未能出现预期波动,逐步亏损的经历也会相当痛苦。这并非为做多或做空跨式期权背书,在适当条件下,两者皆可能是合理的选择。明智的交易者应关注总预期收益,如果最高预期回报的策略伴随无限风险,那么可能需要将这种风险视为交易的一部分。

STRANGLE

勒式期权

Like a straddle, a strangle consists of a long call and a long put, or a short call and a short put, where both options expire at the same time. In a strangle, however, the options have different exercise prices. If both options are purchased, the trader is long the strangle; if both options are sold, the trader is short the strangle. Typical long and short strangles are shown in Figures 8-7 and 8-8.

勒式期权与跨式期权相似,由一个看涨期权和一个看跌期权组成,且两者到期时间相同,但行权价不同。如果买入看涨和看跌期权则称为做多勒式期权;卖出则称为做空勒式期权。典型的多头和空头勒式期权如图8-7和图8-8所示。

Strangles have characteristics similar to straddles, and are therefore similar to backspreads and ratio vertical spreads. Like a long straddle, a long strangle needs movement to be profitable, and has unlimited profit potential should such movement occur. Like a short straddle, a short strangle has unlimited risk in either direction, but will show a profit if the underlying market remains in a narrow trading range.

勒式期权的特征类似于跨式期权,因此也接近反向价差和比率垂直价差。做多勒式期权如同做多跨式期权,需要市场波动才能获利,且在出现波动时具有无限的利润潜力。而做空勒式期权则与做空跨式期权相似,存在上下行无限风险,但若市场保持窄幅波动则可获利。

If a strangle is simply identified by its expiration month and exercise prices, there may be some confusion as to the specific options involved. A June 95/105 strangle might consist of a June 95 put and June 105 call. But it might also consist of a June 95 call and a June 105 put. Both these combinations are consistent with the definition of a strangle. To avoid confusion a strangle is commonly assumed to consist of out-of-the-money options. If the underlying market is currently at 100 and a trader wants to purchase the June 95/105 strangle, it is assumed that he wants to purchase a June 95 put and a June 105 call. When both options are in-the-money, the position is sometimes referred to as a guts.

仅按到期月份和行权价标识勒式期权时,可能对涉及的具体期权产生一些混淆。例如,一个6月95/105勒式期权可能包含6月95看跌期权和6月105看涨期权,也可能包括6月95看涨期权和6月105看跌期权。为避免混淆,通常假设勒式期权由价外期权组成。如果当前市场在100点,而交易者希望买入6月95/105勒式期权,则假设他会买入6月95看跌和6月105看涨期权。当两个期权均为价内时,这种组合有时被称为“实式期权”。

In the absence of other identifying information, strangles, like straddles, are usually executed with a one-to-one ratio (one call for each put). However, there is no law against executing a strangle with some other ratio. If the call has a delta of 15 and the put has a delta of -30, and a trader wants to be delta neutral, it is perfectly acceptable to trade two calls for each put.

如无额外说明,勒式期权通常按一比一比例执行(一个看涨对应一个看跌),但也可以采用其他比例。如果看涨期权delta为15,看跌期权delta为-30,而交易者希望实现delta中性,完全可以按两份看涨对一份看跌的比例进行交易。

If we ignore the limited or unlimited risk/reward characteristics of backspreads, long straddles, and long strangles, these spreads essentially differ in the degree of desired movement. A backspread needs some market movement to show a profit, a long straddle needs more movement, and a long strangle needs even greater movement. Indeed, a strangle is usually considered the most highly leveraged of all option positions because out-of-the-money options are cheap relative to other options. Several strangles can often be purchased for the price of just one straddle. If significant movement occurs with such a position, its value can increase dramatically. But there is a tradeoff. If movement fails to occur, the position will swiftly lose its value through the passage of time.

如果忽略风险/收益的大小,反向价差、做多跨式期权和做多勒式期权的区别主要在于所需波动的程度。反向价差需要一些波动才能盈利,做多跨式期权需要更大波动,而做多勒式期权则需要更大幅度的波动。勒式期权通常被视为杠杆最大的期权,因为价外期权相对便宜,因此多个勒式期权的成本可与单个跨式期权相当。如果市场剧烈波动,其价值将大幅增长,但如果市场不动,价值会迅速因时间流逝而缩水。

The same considerations of degree are also true for ratio vertical spreads, short straddles, and short strangles. A ratio vertical spread, a short straddle, and a short strangle all want the market to sit still. But again, the strangle is considered the most highly leveraged of these positions. If a trader sells several strangles and the market does sit still his profits will usually be greater than if he had sold one straddle or done a moderate sized ratio vertical spread. If, however, the market makes an unexpectedly large move, short strangles also entail the greatest risk. All option positions are a tradeoff between risk and reward. If the reward is great, so is the risk; if the risk is small, so is the reward.

相同的逻辑也适用于比率垂直价差、做空跨式期权和做空勒式期权。比率垂直价差、做空跨式和勒式期权都希望市场保持稳定,但勒式期权仍被认为是其中杠杆最高的。如果交易者卖出多个勒式期权且市场不动,通常利润会比卖出单个跨式期权或适中规模的比率垂直价差更大。但如果市场意外剧烈波动,做空勒式期权也承担最大风险。所有期权头寸都在风险和收益之间取舍,收益越高风险越大,反之亦然。

Based on their similar characteristics, it is sometimes convenient to classify long straddles and long strangles as special types of backspreads. This follows logically from the definition of a backspread: long more contracts than short, with all options expiring in the same month. A long straddle or strangle consists only of long options (long calls and long puts), with all options expiring at the same time. Hence, these positions are backspreads. (Even though the owner of a put has a short market position, he is said to be long the put because he has purchased it.)

基于相似特征,通常将做多跨式期权和勒式期权视为特殊的反向价差。这是因为反向价差的定义是买入期权数量多于卖出期权,且所有期权同月到期。做多跨式和勒式期权仅包含到期日一致的多头期权(看涨和看跌),因此符合反向价差的定义。(尽管看跌期权持有者在市场中持空头头寸,因其买入该期权,仍视为持有看跌多头。)

The same reasoning leads us to classify short straddles and strangles as special types of ratio vertical spreads. Short straddles and strangles consist only of short options, with all options expiring at the same time. Hence, the positions conform to our definition of a ratio vertical spread.

同理,做空跨式和勒式期权可视为特殊的比率垂直价差。它们仅包含空头期权,且所有期权同月到期,因此也符合比率垂直价差的定义。

BUTTERFLY

蝶式价差

Thus far we have looked at spreads which involve buying or selling two different option contracts. However, we need not restrict ourselves to two-sided spreads. We can also construct spreads consisting of three, four, or even more different options. A butterfly consists of options at three equally spaced exercise prices, where all options are of the same type (either all calls or all puts) and expire at the same time. In a long butterfly the outside exercise prices are purchased and the inside exercise price is sold, and vice versa for a short butterfly. (footnote 1: The inside exercise price is sometimes referred to as the body of the butterfly, while the outside exercise prices are referred to as the wings.) Moreover, the ratio of a butterfly never varies. It is always 1 × 2 x 1, with two of each inside exercise price traded for each one of the outside exercise prices. If the ratio is other than 1 x 2 x 1, the spread is no longer a butterfly. Typical examples of long and short butterflies are shown in Figures 8-9 and 8-10.

至今我们讨论的价差策略都涉及买入或卖出两个不同的期权合约。实际上,我们并不局限于双边价差,还可以构建包含三、四甚至更多不同期权的组合。蝶式价差包含三个等距执行价格的期权,所有期权类型一致(均为看涨期权或看跌期权),且到期时间相同。在多头蝶式价差中,外部执行价格期权被买入,中间执行价格期权被卖出;而在空头蝶式价差中则相反。(脚注1:中间执行价格通常称为“蝶身”,外部执行价格称为“蝶翼”)。此外,蝶式价差的比例始终为1×2×1,即每个外部执行价格各有一个合约,而中间执行价格有两个。比例一旦偏离1×2×1,就不再是蝶式价差。图8-9和图8-10展示了典型的多头和空头蝶式价差。

Since a butterfly consists of equal numbers of long and short options, it does not fit conveniently into the backspread or ratio vertical spread category. However, as commonly traded, a long butterfly tends to act like a ratio vertical spread and a short butterfly tends to act like a backspread. To understand why, consider a trader who buys a 95/100/105 call butterfly (long a 95 call, short two 100 calls, long a 105 call). What will be the value of this position at expiration? If the underlying contract is below 95 at expiration all the calls will expire worthless, and the value of the position will be zero. If the underlying contract is above 105 at expiration, the value of the 95 and 105 calls together will be identical to the value of the two 100 calls. Again, the value of the butterfly will be zero. Now suppose the underlying contract is somewhere between 95 and 105 at expiration, specifically, right at the inside exercise price of 100. The 95 call will be worth 5 points, while the 100 and 105 calls will be worthless. The position will therefore be worth 5 points. If the underlying moves away from 100 the value of the butterfly will decline, but its value can never fall below zero.

由于蝶式价差包含相等数量的多头和空头期权,不便归入反向价差或比例垂直价差类别。然而,通常情况下,多头蝶式价差倾向于表现为比例垂直价差,而空头蝶式价差更像反向价差。为理解这一点,假设某交易者买入一个95/100/105看涨期权蝶式价差(多头95看涨期权,空头两个100看涨期权,多头105看涨期权)。到期时,如果标的价格低于95,则所有看涨期权均作废,蝶式价差价值为零;如果标的价格高于105,95和105的看涨期权价值与两个100看涨期权相同,蝶式价差价值同样为零。若标的价格在95到105之间,特别是正好在中间执行价格100,95看涨期权价值为5点,100和105看涨期权价值为零,蝶式价差此时价值为5点。若标的偏离100,则蝶式价差价值会下降,但不会低于零。

At expiration a butterfly will always have a value somewhere between zero and the amount between exercise prices. It will be worth zero if the underlying contract is below the lowest exercise price or above the highest exercise price, and it will be worth its maximum if the underlying contract is right at the inside exercise price.

到期时,蝶式价差的价值总在零到执行价差额之间。若标的价格低于最低执行价或高于最高执行价,则蝶式价差价值为零;若标的价格正好处于中间执行价,则达到最高价值。

Since a butterfly has a value between zero and the amount between exercise prices (5 points in our example), a trader should be willing to pay some amount between zero and 5 for the position. The exact amount depends on the likelihood of the underlying contract finishing right at or close to the inside price at expiration. If there is high probability of this occurring, a trader might be willing to pay as much as 4/4 or 4/2 for the butterfly, since it might very will expand to its full value of 5 points. If, however, there is a low probability of this occurring, and consequently a high probability that the underlying contract will finish outside the extreme exercise prices, a trader may only be willing to pay ½ or ¾, since he may very will lose his entire investment.

由于蝶式价差价值在零与执行价差额(如本例中的5点)之间波动,交易者可能会支付0到5点之间的某个价格,具体取决于标的价格到期时接近中间执行价的概率。若概率高,交易者可能会支付接近4;若概率低,则可能只支付1/2或3/4,因为他可能会损失全部投资。

Now we can see why a long butterfly tends to act like a ratio vertical spread. If a trader feels that the underlying contract will remain within a narrow range until expiration, he can buy a butterfly where the inside exercise price is at-the-money. If he is right, and the market does stay close to the inside exercise price, the butterfly will expand to its maximum value (Figure 8-9). A long butterfly tends to act like a ratio vertical spread since it increases in value as the underlying market sits still.

多头蝶式价差通常表现类似比例垂直价差。若交易者认为标的将在狭窄区间波动,他可以在平值执行价格处买入蝶式价差。如果判断正确且市场接近中间执行价,则蝶式价差会达到最高价值(见图8-9)。因此,多头蝶式价差在标的价格保持不变时增值。

In contrast, the trader who sells a butterfly wants the underlying market to move as far away from the inside exercise price as possible so that the position will expire with the underlying contract either below the lowest exercise price or above the highest exercise price. In this case, the butterfly will expire worthless and he will be able to keep the full amount he received when he sold the butterfly (Figure 8-10). A short butterfly tends to act like a backspread since it increases in value with movement in the underlying market.

相反,卖出蝶式价差的交易者希望标的价格远离中间执行价,使得蝶式价差在标的价格低于最低或高于最高执行价时到期作废,从而保留全部卖出蝶式价差的收入(见图8-10)。空头蝶式价差表现类似反向价差,因为标的价格波动增大时其价值增加。

Why are the strategies in Figure 8-9 referred to as "long" butterflies, and the strategies in Figure 8-10 referred to as "short" butterflies? It is common practice to refer to a spread which requires an outlay of capital as a long, or purchased, spread. If a trader initiates a butterfly by purchasing the outside exercise prices and selling the inside exercise price, he has a position which can never be worth less than zero at expiration. The trader can therefore expect to lay out some amount of capital for the position when he initiates it. When the trader does this, he has purchased, or is "long," the butterfly. (If a trader can initiate a long butterfly for a credit, he should do it as many times as the law will allow; he can't lose.) When the trader sells the outside exercise prices and purchases the inside exercise price, he can expect to receive some amount of capital. He has sold, or is "short," the butterfly.

为什么图8-9中的策略称为“多头”蝶式价差,而图8-10称为“空头”蝶式价差?通常,需支付资本的价差称为多头或买入价差。若交易者通过买入外部执行价、卖出中间执行价建仓,他获得的仓位到期时价值不会低于零,因此需要支付一定成本。当交易者这样操作时,他即持有或“多头”蝶式价差。(若交易者能以信用差建立多头蝶式价差,应尽可能多次交易,因为他不会亏损。)当交易者卖出外部执行价、买入中间执行价时,他会收到一定金额,即“空头”蝶式价差。

Since all butterflies are worth their maximum amount when the underlying contract is right at the inside exercise price at expiration, both a call and put butterfly with the same exercise prices and the same expiration date desire exactly the same outcome, and therefore have identical characteristics. Both the March 95/100/105 call butterfly and the March 95/100/105 put butterfly will be worth a maximum of 5 with the underlying contract right at 100 at expiration, and a minimum value of zero with the underlying contract below 95 or above 105. If both butterflies are not trading at the same price, there is a sure profit opportunity available by purchasing the cheaper and selling the more expensive. (footnote 2: This is not necessarily the case if the spreads consist of American options, where there is a possibility of early exercise. A sure profit would exist only if one were certain of carrying the position to expiration.)

由于所有蝶式价差在到期时,标的价格位于中间执行价时达到最大价值,因此相同执行价和到期日的看涨和看跌蝶式价差追求的目标完全一致,特性也相同。例如,3月95/100/105的看涨和看跌蝶式价差在标的价格恰好为100时最大价值为5,低于95或高于105时最小价值为零。如果这两个蝶式价差的交易价格不同,可通过买入便宜的、卖出较贵的套利。(脚注2:若为美式期权,可能存在提前行权风险,仅在确保持仓至到期时才有稳妥的套利机会。)

If a trader foresees a quiet market, why might he choose a long butterfly over some other type of strategy, for example a short straddle? An important characteristic of a butterfly is its limited risk. If a trader initiates a long butterfly in the belief that the market is unlikely to move very far from the current price, the most he can lose if he is wrong is the amount he laid out to purchase the butterfly. On the other hand, if a trader sells a straddle and the market makes a large move, his potential risk is unlimited. Regardless of theoretical considerations, some traders are not comfortable with the possibility of unlimited risk. If given the choice between purchasing butterflies and selling straddles, they will prefer the former strategy to the latter.

若交易者预计市场平静,为什么选择多头蝶式价差而非其他策略,例如空头跨式价差?蝶式价差的关键特性在于其风险有限。若交易者认为市场不会远离当前价格,选择多头蝶式价差,则他最多损失建仓成本;而若选择空头跨式价差,市场大幅波动时潜在风险无限。即便从理论上看,某些交易者并不接受无限风险,在蝶式价差和跨式价差间,通常会选择前者。

Of course the straddle, while riskier, also has greater profit potential. If a trader intends to purchase butterflies but wants a potential profit commensurate with that of a short straddle, he will have to trade butterflies in much greater size. A trader who is considering the sale of 25 straddles might decide instead to buy 100 butterflies (100 x 200 × 100). While trading 100 spreads may appear riskier than trading 25 spreads, 100 butterflies may in fact be much less risky than 25 straddles because of the risk characteristics associated with a butterfly. A trader should never confuse size and risk. Risk often depends on the characteristics of the strategy, not on the size in which the strategy is executed.

当然,跨式价差风险更高,利润潜力也更大。若交易者希望蝶式价差具备类似空头跨式价差的潜在收益,则需大规模交易。比如,计划卖出25个跨式价差的交易者可能考虑买入100个蝶式价差(100 x 200 x 100)。虽然交易100个价差看似风险较大,但蝶式价差的风险特性决定了其实际风险可能低于25个跨式价差。交易者应避免将规模等同于风险,风险取决于策略特性,而非策略规模。

TIME SPREAD

时间价差

(also referred to as a calendar spread or horizontal spread)

(也称为日历价差或水平价差)

If all options in a spread expire at the same time, the value of the spread is simply a function of the underlying price at expiration. If, however, the spread consists of options which expire at different times, the value of the spread cannot be determined until both options expire. The spread's value depends not only on where the underlying market is when the short-term option expires, but also on what will happen between that time and the time when the long-term option expires. Time spreads, sometimes referred to as calendar spreads or horizontal spreads, (footnote 3: Expiration months were originally listed horizontally on exchange option displays. Hence the term horizontal spread.) consist of opposing positions which expire in different months.

如果价差中的所有期权在相同时间到期,其价值仅取决于到期时的标的价格。然而,若价差中的期权到期时间不同,则其价值需等到两个期权都到期后才能确定。价差的价值不仅依赖于短期期权到期时标的市场的价格,还依赖于从该时点到长期期权到期之间的市场走势。时间价差,也称为日历价差或水平价差(脚注3:期权到期月份最初在交易所屏幕上水平排列,因此得名),由不同月份到期的对冲头寸组成。

The most common type of time spread consists of opposing positions in two options of the same type either both calls or both puts where both options have the same exercise price. When the long-term option is purchased and the short-term option is sold, a trader is long the time spread; when the short-term option is purchased and the long-term option is sold, the trader is short the time spread. Since a long-term option will have more time value, and therefore a higher price than a short-term option, this is consistent with the practice of referring to any spread which is executed at a debit (credit) as a long (short) spread position.

最常见的时间价差是具有相同执行价的两个对冲头寸,且类型相同(都为看涨期权或看跌期权)。当买入长期期权并卖出短期期权时,称为多头时间价差;当买入短期期权并卖出长期期权时,则称为空头时间价差。由于长期期权包含更多时间价值,其价格通常高于短期期权,这与以借记(贷记)执行的价差被称为多头(空头)价差的惯例一致。

Although time spreads are most commonly executed one-to-one (one contract purchased for each contract sold), a trader may ratio a time spread to reflect a bullish, bearish, or neutral market sentiment. For the present we will assume that all time spreads will be ratioed delta neutral. Typical long and short time spreads are shown in Figures 8-11 and 8-12.

虽然时间价差通常以一对一(买入一个合约对应卖出一个合约)形式执行,但交易者也可根据市场情绪(看涨、看跌或中性)调整时间价差的比例。此处我们假设所有时间价差均保持Delta中性。典型的多头和空头时间价差示例见图8-11和8-12。

A time spread has different characteristics from the other spreads we have discussed, because its value depends not only on movement in the underlying market, but also on other traders' expectations about future market movement as reflected in the implied volatility. If we assume that the options making up a time spread are approximately at-the-money, time spreads have two important characteristics.

时间价差与其他价差有不同特性,因为其价值不仅受标的市场波动影响,还受到其他交易者对未来市场波动的预期,即隐含波动率的影响。如果假设构成时间价差的期权接近平值,时间价差具有两个重要特性。

A long time spread always wants the underlying market to sit still. An important characteristic of an at-the-money option's theta (time decay) is its tendency to become increasingly large as expiration approaches. As time passes, a short term at-the-money option, having less time to expiration, will lose its value at a greater rate than a long-term at-the-money option. (Note the value of at-the-money options in Figures 6-13 and 6-14, and the theta values in Figure 6-15.) This principle has an important effect on the value of a time spread.

多头时间价差希望标的市场保持稳定。平值期权的theta(时间衰减)有一个重要特性:随着到期时间的临近,其theta值会逐渐增大。随着时间推移,短期期权因到期时间较短,价值损失速度大于长期期权(参见图6-13和6-14中的平值期权价值,以及图6-15中的theta值)。这一原则对时间价差的价值有重要影响。

For example, suppose two at-the-money calls, one with three months to expiration and one with six months to expiration, have values of 6 and 7½, respectively. The value of the spread is therefore 1½. If one month passes and the underlying market is unchanged, both options will lose value. But the short-term option, with its greater theta, will lose a greater amount. If the long-term option loses /, the short-term option may lose a full point. Now the options are worth 5 and 7¼, and the spread is worth 2¼. If another month passes and the market is still unchanged, both options will continue to decay, But, again, the short-term option, with less time remaining to expiration, will decay at a greater rate. If the long-term option loses ½, the short term option may lose 2 points. Now the options are worth 3 and 6¼, and the spread has increased in value to 3¾. Finally, if at expiration the market is still unchanged, the short-term option, since it is still at-the-money, will lose all of its remaining value of 3 points. The long-term option will continue to decay but will do so at a slower rate. If the long-term option loses ¾, it will be worth 6 points, and the spread will be worth 6 points (Figure 8-13).

例如,假设有两个平值看涨期权,一个到期时间为三个月,另一个为六个月,价值分别为6和7½。因此,价差为1½。如果经过一个月,标的市场不变,两个期权都会贬值,但短期期权因theta值较大,贬值幅度会更大。如果长期期权贬值½,短期期权可能贬值整整1点。此时,期权的价值为5和6¼,价差增至2¼。如果再经过一个月,市场仍然不变,两个期权将继续贬值,但短期期权贬值速度仍较快。如果长期期权贬值½,短期期权可能贬值2点。此时,期权的价值为3和4¼,价差增加到3¼。最后,如果到期时市场仍然不变,短期期权因仍为平值,将失去剩余的3点价值。长期期权将继续贬值,但速度较慢。如果长期期权贬值¾,将价值降至6点,价差将值为6点(见图8-13)。

What will happen if the underlying market makes a larger move? Assume as before that both options are at-the-money and have values of 7½ and 6. As the underlying market rises and options move more deeply into-the-money, they begin to lose their time value. If the move is large enough, it won't matter that the long-term option has three more months remaining to expiration. Both options will eventually lose all their time value (see Figures 6-15 and 6-16). If the time spread consists of calls, both of which have exercise prices of 100, and the underlying market moves from 100 to 150, both options might trade at parity (intrinsic value), or 50 points. The spread will then go to zero. Even if the long term option retains as much as ¼ point, the spread will still have collapsed to ¼.

如果标的市场发生较大波动会怎样?假设两者仍为平值期权,价值分别为7½和6。当标的市场上涨且期权深入到期内时,它们开始失去时间价值。如果波动幅度足够大,长期期权还有三个月到期的情况也无关紧要。两个期权最终会失去所有时间价值(见图6-15和6-16)。如果时间价差由执行价格为100的看涨期权组成,而标的市场从100涨至150,则两个期权的交易价可能会平价(内在价值),即50点。此时,价差将归零。即使长期期权仍保留¼点,价差也将减少至¼。

What about a large downward move in the underlying market? The situation is almost identical to an upward move. As an option moves further out-of-the-money its time value also begins to shrink. Here, however, neither option will have any intrinsic value, so that if the market moves down far enough both options will eventually be worthless. If that happens, the time spread will be worthless. If, as above, the long-term option retains even ¼ point in value, the spread will still collapse to /4 point.

如果标的市场发生较大下跌,情况几乎与上涨时相同。当期权进一步变为虚值时,其时间价值也开始缩小。然而,此时两个期权都没有内在价值,如果市场下跌足够多,两个期权最终将毫无价值。如果发生这种情况,时间价差也将毫无价值。如果长期期权仍然保留¼点的价值,价差依然会跌至¼点。

Since a short-term at-the-money option always decays more quickly than a long-term at-the-money option, regardless of whether the options are calls or puts, both a long call time spread and a long put time spread want the underlying market to sit still. Ideally, both spreads would like the short-term option to expire right at-the-money so that the long-term option will retain as much time value as possible while the short-term option expires worthless.

由于短期期权的贬值速度总是快于长期期权,无论是看涨期权还是看跌期权,长看涨时间价差和长看跌时间价差都希望标的市场保持稳定。理想情况下,两个价差都希望短期期权在到期时正好为平值,以便长期期权保留尽可能多的时间价值,而短期期权则毫无价值到期。

If a long time spread wants the market to sit still, logically a short time spread wants the market to move. It may therefore seem that, as with backspreads and ratio vertical spreads, the major consideration in deciding whether to initiate a long or short time spread is the likelihood of movement in the underlying market. Certainly time spreads are sensitive to movement in the price of the underlying, but time spreads are also sensitive to changes in implied volatility.

如果长时间价差希望市场保持稳定,那么短时间价差自然希望市场发生波动。因此,似乎与反向价差和比率垂直价差一样,决定是启动长时间价差还是短时间价差的主要考虑因素是标的市场的波动可能性。毫无疑问,时间价差对标的价格的波动非常敏感,但时间价差同样也对隐含波动率的变化敏感。

A long time spread always benefits from an increase in implied volatility. Look again at Figure 6-18, the relationship between an option's vega (sensitivity to a change in volatility) and the time remaining to expiration. As time to expiration increases, the vega of an option increases. This means that a long-term option is always more sensitive in total points to a change in volatility than a short-term option with the same exercise price.

长时间价差总是受益于隐含波动率的增加。再看看图6-18,期权的维加(对波动率变化的敏感度)与剩余到期时间之间的关系。随着到期时间的增加,期权的维加也会增加。这意味着,长期期权对波动率变化的总点数敏感度总是高于同一执行价格的短期期权。

For example, assume again that a 100 call time spread is worth 1½ (long- and short-term options with values of 7/2 and 6, respectively). Assume also that the value of the spread is based on a volatility of 20%. What will happen to the value of the spread if we raise volatility to 25%? Both options will increase in value since an increase in volatility increases the value of all options. But the long-term option, with more time remaining to expiration and therefore a higher vega, will gain more value as a result of the increase in volatility. If the short-term option gains /2, the long-term option may gain a full point. Now the options will be worth 8½ and 6/, and the spread will have widened from 1½ to 2 (Figure 8-14).

例如,假设100的看涨时间价差值为1½(长期和短期期权的价值分别为7/2和6)。假设该价差的价值是基于20%的波动率。如果我们将波动率提高到25%,价差的价值会发生什么变化?由于波动率的增加会提升所有期权的价值,因此两个期权的价值都会上升。但由于长期期权还有更多的到期时间,维加也更高,因此它的价值增长会更明显。如果短期期权增加了¼点,长期期权可能会增加1点。此时,期权的价值将变为8½和6/,价差从1½扩大到2(图8-14)。

Conversely, if we lower our volatility estimate to 15%, both options will lose value. But the long-term option, with more time remaining to expiration, will be more sensitive to the change in volatility and will lose a greater amount. The new option values might be 6½ and 5½, causing the spread to narrow to 1 point.

反之,如果我们将波动率估计降低到15%,两个期权的价值都会下降。但由于长期期权有更多的到期时间,对波动率变化更敏感,因此损失会更大。新期权的价值可能会变为6½和5½,导致价差缩小到1点。

The effects of volatility on a time spread become especially evident when there is a change in implied volatility in the option market. When implied volatility rises, time spreads tend to widen; when implied volatility falls, time spreads tend to narrow. This effect can often be great enough to offset either a favorable or unfavorable move in the underlying market. A trader who is long a time spread expects to lose money if the underlying market makes a swift move in either direction. He knows that time spreads begin to collapse as the options move into- or out-of-the-money. But if this movement is accompanied by a sufficient increase in implied volatility, the increase in the spread's price due to the increase in implied volatility may actually be greater than the loss due to market movement. In that case the trader may find that the spread has actually widened. Conversely, if the market sits still, the trader expects the spread to widen because of the short-term option's greater time decay. But if, at the same time, there is a collapse in implied volatility, the decline in the spread's price due to the decline in implied volatility may more than offset any gain from the passage of time. If this happens, the trader may find that the spread has narrowed.

波动率对时间价差的影响在隐含波动率发生变化时尤为明显。当隐含波动率上升时,时间价差往往会扩大;而当隐含波动率下降时,时间价差则趋于缩小。这种影响往往足以抵消市场的有利或不利变动。持有时间价差的交易者预计,如果基础市场快速变动,他们会亏损。他们知道,随着期权进入或脱离价内,时间价差会开始收缩。但如果这种变动伴随着隐含波动率的显著上升,因隐含波动率上升而导致的价差上涨可能超过因市场波动造成的损失。在这种情况下,交易者可能会发现价差实际上已经扩大。相反,如果市场保持不变,交易者预计因短期期权的更快时间衰减,价差会扩大。但如果隐含波动率同时崩溃,因隐含波动率下降导致的价差下跌可能会超过因时间推移带来的收益。这种情况下,交易者可能会发现价差已缩小。

These two opposing forces, the decay in an option's value due to the passage of time and the change in an option's value due to changes in volatility, give time spreads their unique characteristics. When a trader buys or sells a time spread, he is not only attempting to forecast movement in the underlying market. He is also trying to forecast changes in implied volatility. The trader would like to forecast both inputs accurately, but often an error in one input can be offset by an accurate forecast for the other input.

这两种相反的力量——由于时间推移导致的期权价值衰减和由于波动率变化导致的期权价值变化——赋予了时间价差独特的特性。当交易者买入或卖出时间价差时,他们不仅试图预测基础市场的变动,同时也在尝试预测隐含波动率的变化。交易者希望能够准确预测这两个因素,但往往一个因素的错误可以通过另一个因素的准确预测来弥补。

Ideally, the trader who is long a time spread wants two apparently contradictory conditions in the marketplace. First, he wants the underlying market to sit still so that time decay will have a beneficial effect on the spread. Second, he wants everyone to think the market is going to move so that implied volatility will rise. This may seem an impossible scenario, the market remaining unchanged but everyone thinking it will move. In fact, this happens quite often because events which don't have an immediate effect on the underlying market could be perceived to have a future effect on the market.

理想情况下,持有时间价差的交易者希望市场上出现两种看似矛盾的情况。首先,他们希望基础市场保持不变,这样时间衰减对价差会产生积极影响。其次,他们希望大家都认为市场将会变动,从而使隐含波动率上升。这看似是一个不可能的场景:市场保持不变,但大家都认为它会变动。事实上,这种情况常常发生,因为某些事件虽然不会立即影响基础市场,但可能被认为会在未来对市场产生影响。

Suppose an announcement is made that the finance ministers of the major industrialized countries plan to meet to discuss exchange rates. If no one knows what the outcome of the meeting will be, there is unlikely to be any significant move in the currency markets when the initial announcement is made. On the other hand, all traders will assume that major changes in exchange rates could result from the meeting. This possibility will result in an increase in implied volatility in the currency option market. The lack of movement in the underlying market, together with the increase in implied volatility, will cause time spreads to widen.

假设有消息称主要工业化国家的财政部长计划召开会议讨论汇率。如果没有人知道会议的结果,初始公告发布时,货币市场不太可能出现重大波动。另一方面,所有交易者都将假设会议可能导致汇率的重大变化。这种可能性将导致货币期权市场的隐含波动率上升。基础市场的平稳加上隐含波动率的增加,会导致时间价差扩大。

Suppose that, as a result of the meeting, the finance ministers decide to maintain the status quo. Now expectations of a major change in exchange rates fade, implied volatility falls, and, as a result, time spreads narrow.

如果会议结果是财政部长决定维持现状,那么对汇率重大变化的预期将减弱,隐含波动率下降,结果时间价差缩小。

Scenarios with similar consequences also occur in the interest rate options market when a policy statement is expected from the Federal Reserve in the United States, or when a company's earnings are due to be reported in the stock option market. These events are unlikely to have an effect on the underlying market before the fact, but they could have significant repercussions after the fact.

类似的情况也会在利率期权市场发生,比如美国联邦储备委员会即将发布政策声明,或者某公司即将公布财报。这些事件在发生前不太可能影响基础市场,但事后可能会产生重大影响。

The effect of implied volatility is what distinguishes time spreads from the other types of spreads we have discussed. Backspreads (including long straddles, long strangles, and short butterflies) and ratio vertical spreads (including short straddles, short strangles, and long butterflies) want real volatility (price movement in the underlying market) and implied volatility (a reflection of expectations about future price movement in the underlying market) to either both rise or both fall. A swift move in the underlying market or an increase in implied volatility will help a backspread. A quiet market or a decrease in implied volatility will help a ratio vertical spread. With time spreads, however, real and implied volatility have opposite effects. A big move in the underlying market or a decrease in implied volatility will help a short time spread, while a quiet market or an increase in implied volatility will help a long time spread. This opposite effect is what gives time spreads their unique characteristics.

隐含波动率的影响使时间价差与其他类型的价差有所区别。反向价差(包括长期平价、长期跨式和短期蝴蝶价差)及比例垂直价差(包括短期平价、短期跨式和长期蝴蝶价差)希望实际波动率(基础市场的价格波动)和隐含波动率(对未来价格波动的预期)要么同时上升,要么同时下降。基础市场的快速波动或隐含波动率的上升有利于反向价差,而平稳市场或隐含波动率的下降则有利于比例垂直价差。然而,对于时间价差来说,实际波动率和隐含波动率的影响则相反。基础市场的大幅波动或隐含波动率的下降有利于短期时间价差,而平稳市场或隐含波动率的上升则有利于长期时间价差。这种相反的效果赋予了时间价差独特的特性。

While the foregoing characteristics of time spreads apply to all option markets, there may be other considerations, depending on the specific underlying market. We previously assumed that the price of the underlying contract for both the short- and long-term option was the same. In the stock option market this will always be true because the underlying for every expiration is the same stock. The underlying contract for all IBM options, regardless of the expiration month, is always IBM stock. And IBM stock can only have a single price at any one time. In contrast, the underlying for a futures option is a specific futures contract. Consider this situation for Eurodollar futures and options traded at the CME:

March Eurodollar Futures = 93.90

June Eurodollar Futures = 93.75

Suppose a trader initiates a long time spread:

long 10 June 94.00 calls

short 10 March 94.00 calls

虽然上述时间价差的特点适用于所有期权市场,但具体的基础市场可能还有其他考虑因素。我们之前假设短期和长期期权的基础合约价格相同。在股票期权市场中,这始终成立,因为每个到期日的基础资产都是同一只股票。所有IBM期权的基础资产,无论到期月份如何,始终是IBM股票,而IBM股票在任何时候只能有一个价格。相比之下,期货期权的基础资产是特定的期货合约。以下是CME交易的欧元美元期货和期权的情况:

三月欧元美元期货 = 93.90

六月欧元美元期货 = 93.75

假设一位交易员启动了一个长期时间价差:

买入10个六月94.00看涨期权

卖出10个三月94.00看涨期权

The underlying for March Eurodollar options is a March Eurodollar futures con-tract; the underlying for June Eurodollar options is a June Eurodollar futures contract. While the March and June Eurodollar futures contracts are related, they are not identical. It is not impossible for one futures contract to go up while the other goes down. As a result, in addition to volatility considerations, a trader who buys a June/March Eurodollar option call time spread also has to worry about the risk of the June futures contract falling while the March futures contract is rising. Is there any way to offset this risk?

三月欧元美元期权的基础资产是三月欧元美元期货合约,而六月欧元美元期权的基础资产是六月欧元美元期货合约。尽管三月和六月的欧元美元期货合约相关,但并不相同。一个期货合约上涨的同时,另一个期货合约下跌并非不可能。因此,除了波动性考虑外,购买六月/三月欧元美元期权看涨时间价差的交易员还需担心六月期货合约下跌而三月期货合约上涨的风险。有办法来抵消这种风险吗?

If, in our example, the spread between the March and June futures contracts, which is currently. 15, begins to widen, the option spread will narrow regardless of volatility considerations. If, however, when the trader initiates the option spread, he also executes a futures spread by purchasing March futures and selling June futures, he will have a position which will offset any loss to the option spread resulting from a widening in the futures spread.

如果在我们的例子中,三月和六月期货合约的价差当前为0.15,且开始扩大,那么期权价差将缩小,而不论波动性如何。然而,如果交易员在启动期权价差时同时执行期货价差,通过购买三月期货和卖出六月期货,他将持有一个能抵消因期货价差扩大而导致的期权价差损失的头寸。

How many futures spreads should the trader execute? He ought to trade the number of futures spreads required to be delta neutral. If the delta of both options is 40 and the trader executes the option spread ten times, he will be long 400 deltas in June and short 400 deltas in March. Therefore, he should buy 4 March futures contracts and sell 4 June futures contracts. The entire spread will look like this (deltas are in parentheses):

long 10 June 94.00 calls (40) short 4 June futures (100)

short 10 March 94.00 calls (40) long 4 March futures (100)

This type of balancing is not necessary, indeed not possible, in stock options because the underlying for all months is identical. There is no such thing as March IBM stock or June IBM stock.

交易员应该执行多少个期货价差?他应该交易所需数量的期货合约,以保持德尔塔中性。如果两个期权的德尔塔均为40,交易员执行期权价差十次,那么他将在六月持有400德尔塔的多头,而在三月持有400德尔塔的空头。因此,他应购买4个三月期货合约,卖出4个六月期货合约。整个头寸如下(德尔塔值在括号中):

买入10个六月94.00看涨期权(40) 卖出4个六月期货(100)

卖出10个三月94.00看涨期权(40) 买入4个三月期货(100)

在股票期权中,这种平衡是不必要的,实际上也是不可能的,因为所有月份的基础资产是相同的。不存在三月IBM股票或六月IBM股票的说法。

THE EFFECT OF CHANGING INTEREST RATES AND DIVIDENDS

利率和股息变化的影响

Thus far we have considered only the effects of changes in the price of the underlying market and changes in volatility on the value of volatility spreads. What about changes in interest rates and, in the case of stocks, dividends?

到目前为止,我们只考虑了基础市场价格变化和波动性变化对波动性价差的影响。那么,利率变化以及在股票情况下的股息变化又会有什么影响呢?

Because there is no carrying cost associated with the purchase or sale of a futures contract, interest rates have only a minor impact on futures options, and, consequently, a negligible effect on the value of futures option volatility spreads. (footnote 4: Interest rates can of course affect the relative value of different futures months. As noted, we can offset this risk by trading a futures spread along with the futures option time spread.) If, however, we are trading stock options and change the interest rate, we change the forward price of stock (the current stock price plus the carrying cost on the stock to expiration). When all options expire at the same time, as they do in backspreads and ratlo vertical spreads, the forward stock price for all options remains the same, so that the effects of the change are practically negligible. If, on the other hand, we are considering stock options with different expiration dates, we must consider two different forward prices. And these two forward prices may not be equally sensitive to a change in interest rates. For example, consider the following situation:

Stock price = 100 Interest rate = 12% Dividend = 0

Suppose a trader initiates a long time spread:

long 10 June 100 calls

short 10 March 100 calls

由于购买或出售期货合约没有持有成本,利率对期货期权的影响较小,因此对期货期权波动性价差的影响也微乎其微。(脚注4:利率当然会影响不同期货月份的相对价值。如前所述,我们可以通过同时交易期货价差和期货期权时间价差来抵消这一风险。)然而,如果我们在交易股票期权并改变利率,就会改变股票的远期价格(当前股票价格加上到期的持有成本)。当所有期权同时到期时,如在反向价差和比例垂直价差中,所有期权的远期股票价格保持不变,因此变化的影响几乎可以忽略不计。另一方面,如果我们考虑不同到期日的股票期权,则必须考虑两个不同的远期价格。这两个远期价格对利率变化的敏感性可能并不相同。例如,考虑以下情况:

股票价格 = 100 利率 = 12% 股息 = 0

假设交易员启动一个长期价差:

买入10个六月100看涨期权

卖出10个三月100看涨期权

If there are three months remaining to March expiration and six months remaining to June expiration, the forward prices for March and June stock are 103 and 106, respectively. If interest rates drop to 8 percent, the forward price for March will be 102 and the forward price for June will be 104. With more time remaining, the June forward price is more sensitive to a change in interest rates. Assuming the deltas of both options are approximately equal, the June option will be more affected in total points by the decline in interest rates than the March option, and the time spread will narrow. In the same way, if interest rates increase, the time spread will widen because the June forward price will rise more quickly than the March forward price. Therefore, a long (short) call time spread in the stock option market must have a positive (negative rho.

如果距离三月到期还有三个月,距离六月到期还有六个月,则三月和六月的远期价格分别为103和106。如果利率降至8%,三月的远期价格将变为102,六月的远期价格为104。由于时间更长,六月的远期价格对利率变化的敏感性更高。假设两个期权的德尔塔大致相等,则利率下降对六月期权的影响在总点数上大于三月期权,时间价差将缩小。同样,如果利率上升,时间价差将扩大,因为六月的远期价格将比三月的远期价格上涨得更快。因此,在股票期权市场中,长期(短期)看涨期权价差必须具有正(负)rho。

Changes in interest rates have just the opposite effect on stock option puts. In our example, if interest rates fall from 12% to 8% the March forward price will fall from 103 to 102, while the June forward price will fall from 106 to 104. Again, if we assume that the deltas of both options are approximately equal, and recalling that puts have negative deltas, the June put will show a greater increase in value than the March put. The put time spread will therefore widen. In the same way, if interest rates increase, the put time spread will narrow. Therefore, a long (short) put time spread in the stock option market must have a negative (positive) rho.

利率变化对股票期权看跌期权的影响正好相反。在我们的例子中,如果利率从12%降至8%,三月的远期价格将从103降至102,六月的远期价格将从106降至104。同样,假设两个期权的德尔塔大致相等,且看跌期权的德尔塔为负,那么六月看跌期权的价值增长将大于三月看跌期权。因此,看跌期权的时间价差将扩大。同样地,如果利率上升,看跌期权的时间价差将缩小。因此,在股票期权市场中,长期(短期)看跌期权价差必须具有负(正)rho。

The degree to which stock option time spreads are affected by changes in interest rates depends primarily on the amount of time between expiration dates. If there are six months between expiration dates (e.g., March/September) the effect will be much greater than if there is only one month between expiration dates (e.g., March/April).

股票期权时间价差受到利率变化影响的程度主要取决于到期日期之间的时间间隔。如果到期日期之间有六个月(例如,三月/九月),影响将大得多;而如果只有一个月(例如,三月/四月),影响则较小。

Changes in dividends can also affect the value of stock option time spreads. Dividends, however, have the opposite effect on stock options as changes in interest rates (see Chapter 3). An increase (decrease) in dividends lowers (raises) the forward price of stock. If all options in a volatility spread expire at the same time (backspreads, ratio vertical spreads), the forward stock price will be identical for all options and the effect on the spread will be negligible. But in a time spread, if a dividend payment is expected between expiration of the short-term and long-term option, the long-term option will be affected by the lowered forward price of the stock. Hence, an increase in dividends, if at least one dividend payment is expected between the expiration dates, will cause call time spreads to narrow and put time spreads to widen. A decrease in dividends will have the opposite effect, with call time spreads widening and put time spreads narrowing. The effect of changing interest rates and dividends on stock option time spreads is shown in Figure 8-15.

股息的变化也会影响股票期权时间价差的价值。不过,股息与利率变化的影响正好相反(见第三章)。股息的增加(减少)会降低(提高)股票的远期价格。如果波动率价差中的所有期权同时到期(如反向价差、比例垂直价差),则所有期权的远期股票价格相同,对价差的影响可以忽略不计。但在时间价差中,如果预期在短期期权和长期期权到期之间有股息支付,长期期权会受到降低的远期股票价格的影响。因此,如果在到期日期之间预期至少有一次股息支付,股息的增加将导致看涨期权的时间价差缩小,而看跌期权的时间价差扩大。股息的减少则会产生相反的效果,导致看涨期权的时间价差扩大,看跌期权的时间价差缩小。利率和股息变化对股票期权时间价差的影响如图8-15所示。

Even if both options are deeply in-the-money, a call time spread in the stock option market should always have some value greater than zero. If volatility is very low, the spread should still be worth a minimum of the cost of carry on the stock between expiration months. This is only true, however, if a trader can carry a short stock position between expiration months. If a situation arises where no stock can be borrowed, the trader who owns a time spread may be forced to exercise his long-term option, thereby losing the time value associated with the option.

即使两个期权都深度实值,股票期权市场中的看涨期权时间价差也应始终具有大于零的价值。如果波动率非常低,该价差至少应值于到期月份之间的持有成本。然而,这仅在交易者能够在到期月份之间持有空头股票头寸的情况下才成立。如果出现无法借入股票的情况,持有时间价差的交易者可能被迫行使其长期期权,从而失去与期权相关的时间价值。

As an example, suppose in February a company's stock is trading at 70, when a tender offer is made to buy a portion of the outstanding stock at a price of 80. If a trader is long a June/March 70 call time spread, he will be assigned on the March 70 call because the holder of that call wants to tender his stock for sale at 80. The trader is now short stock and long a June 70 call. The June call should still carry some time value because of the interest which can be earned on the short stock to June expiration. But in order to carry a short stock position, the trader must deliver the stock to the exerciser of the March 70 call. To deliver the stock, he must borrow it from someone. Unfortunately, no one will lend stock to the trader because everyone wants to tender the stock for sale at the tender price of 80. Unless the trader wants to go into the market and buy the stock at the tender price of 80, he will be forced to exercise his June 70 call. This is the only method by which the trader can obtain stock for delivery to the exerciser of the March 70 call. Even though the June 70 call should in theory have some time value, the trader will be forced to discard the time value in order to fulfill his delivery obligation.

举个例子,假设在二月,一家公司的股票交易价格为70,此时公司发出收购要约,以80的价格购买部分流通股。如果一名交易者持有六月/三月70的看涨期权时间价差,他会在三月70的看涨期权上被分配,因为持有该期权的人希望以80的价格出售股票。此时,交易者变成了短仓股票并持有六月70的看涨期权。由于短仓股票在六月到期前可以赚取利息,因此六月期权仍应有一定的时间价值。但为了持有短仓股票,交易者必须将股票交付给行使三月70看涨期权的人。为此,他需要从别人那里借入股票。不幸的是,没人愿意借股票给交易者,因为大家都想以80的价格出售股票。除非交易者愿意以80的价格在市场上购买股票,否则他将被迫行使自己的六月70看涨期权。这是交易者获取股票并交付给行使三月70看涨期权的唯一方法。尽管理论上六月70看涨期权应该有一些时间价值,但交易者为了履行交付义务,不得不放弃这部分时间价值。

In the foregoing situation, sometimes referred to as a short squeeze, a trader is forced to exercise calls with some time value remaining because no stock can be borrowed to carry a short stock position. Anyone who owns the June/March 70 call time spread will be forced to exercise the June 70 call, and the price of the time spread will collapse to zero. Note that this situation is not the same as a buy-out, where all the stock in a company is purchased at one price. Although a tender offer was made at 80, it was for only a portion of the company's outstanding stock. When the tender is completed, the remaining stock will continue to trade, most likely at its pre-tender price of 70.

在上述情况下,有时被称为“逼空”,交易者被迫行使仍有一些时间价值的看涨期权,因为无法借入股票以持有短仓。任何拥有六月/三月70看涨期权时间价差的人都将被迫行使六月70的看涨期权,而时间价差的价格将崩溃至零。需要注意的是,这种情况与收购不同,收购是以一个价格购买公司所有股票。虽然以80的价格发出了收购要约,但仅针对公司部分流通股。当收购完成后,剩余股票将继续交易,价格最有可能回到收购前的70。

DIAGONAL SPREADS

对角价差

A diagonal spread is similar to a time spread, except that the options have different exercise prices. While many diagonal spreads are executed one-to-one (one long-term option for each short-term option), diagonal spreads can also be ratioed, with unequal numbers of long and short market contracts. With the large number of variations in diagonal spreads, it is almost impossible to generalize about their characteristics as we can with backspreads, ratio vertical spreads, and long and short time spreads. Each diagonal spread must be analyzed separately, often using a computer, to determine the risks and rewards associated with the spread.

对角价差类似于时间价差,但期权的行使价格不同。尽管许多对角价差是以一对一的方式执行(每个短期期权对应一个长期期权),对角价差也可以采用不同比例,即长期和短期合约的数量不相等。由于对角价差有很多变化,几乎不可能像处理反向价差、比率垂直价差和长期与短期时间价差那样对其特征进行概括。每个对角价差都必须单独分析,通常需要使用计算机来确定相关的风险和收益。

There is, however, one type of diagonal spread about which we can generalize. If a diagonal spread is done one-to-one, and both options are of the same type and have approximately the same delta, the diagonal spread will act very much like a conventional time spread. An example of a such diagonal spread is shown in Figure 8-12.

不过,有一种类型的对角价差可以进行概括。如果对角价差是以一对一的方式进行,并且两个期权类型相同且delta大致相同,那么该对角价差将表现得非常像传统的时间价差。图8-12中展示了一个这样的对角价差示例。

OTHER VARIATIONS

其他变体

The spreads we have thus far defined are the primary types of volatility spreads, and are the ones most commonly executed in the marketplace. There are, however, some variations of which the reader ought to be aware.

到目前为止,我们定义的价差是主要的波动性价差类型,也是市场上最常见的交易方式。然而,还有一些变体读者应当了解。

A Christmas tree (also referred to as a ladder) is a term which can be applied to a variety of spreads. The spread usually consists of three different exercise prices where all options are of the same type and expire at the same time. In a long (short) call Christmas tree, one call is purchased (sold) at the lowest exercise price, and one call is sold (purchased) at each of the higher exercise prices. In a long (short) put Christmas tree, one put is purchased (sold) at the highest exercise price, and one put is sold (purchased) at each of the lower exercise prices. Christmas trees are usually delta neutral, but even with this restriction, there are many ways to execute the spread. Some examples of Christmas trees are shown in Figure 8-16.

圣诞树差价(也称为梯形价差)是一个可以用于多种价差的术语。该价差通常由三个不同的行使价格组成,所有期权类型相同并在同一时间到期。在长期(短期)看涨圣诞树中,以最低的行使价格购买(卖出)一份看涨期权,并在每个更高的行使价格上卖出(购买)一份看涨期权。在长期(短期)看跌圣诞树中,以最高的行使价格购买(卖出)一份看跌期权,并在每个更低的行使价格上卖出(购买)一份看跌期权。圣诞树差价通常是delta中性的,但即使有这个限制,执行这种价差仍有许多方式。图8-16展示了一些圣诞树的示例。

Long Christmas trees, when done delta neutral, can be thought of as particular types of ratio vertical spreads. Such spreads therefore increase in value if the underlying market either sits still or moves very slowly. Short Christmas trees can be thought of as particular types of backspreads, and therefore increase in value with big moves in the underlying market.

当做多圣诞树以delta中性方式进行时,可以视为特定类型的比率垂直价差。这类价差的价值会随着标的市场的静止或缓慢波动而增加。做空圣诞树可以视为特定类型的反向价差,因此在标的市场大幅波动时,价值会增加。

It is possible to construct a spread which has the same characteristics as a butterfly by purchasing a straddle (strangle) and selling a strangle (straddle) where the straddle is executed at an exercise price midway between the strangle's exercise prices. All options must expire at the same time. Because the position wants the same outcome as a butterfly, it is known as an iron butterfly. Like a true butterfly, at expiration an iron butterfly has a minimum value of zero and a maximum value of the amount between exercise prices.

可以通过购买一个跨式期权(straddle)并卖出一个跨式期权(strangle),其中跨式期权的行使价格位于跨式期权行使价格之间,来构建具有蝴蝶价差特征的价差。所有期权必须同时到期。由于该头寸希望达到与蝴蝶价差相同的结果,因此称为铁蝴蝶。与真正的蝴蝶价差一样,在到期时,铁蝴蝶的最小价值为零,最大价值为行使价格之间的金额。

Note that if the straddle is purchased and the strangle is sold, the position will result in a debit (a long iron butterfly). Such a position will show its greatest profit at expiration if the underlying market finishes beyond the outside (strangle's) exercise prices. A long iron butterfly is therefore equivalent to a short butterfly. If the straddle is sold and the strangle is purchased, the position will result in a debit (a short iron butterfly). Such a position will show its greatest profit at expiration if the underlying market finishes right at the inside (straddle's) exercise price. A short iron butterfly is therefore equivalent to a long butterfly. Examples of long and short iron butterflies are shown in Figure 8-17.

注意,如果购买跨式期权并卖出跨式期权,头寸将产生借记(即长期铁蝴蝶)。如果标的市场在到期时超出外部(跨式期权的)行使价格,该头寸将显示最大利润。因此,长期铁蝴蝶等同于短期蝴蝶。如果卖出跨式期权并购买跨式期权,头寸将产生借记(即短期铁蝴蝶)。如果标的市场在到期时正好位于内部(跨式期权的)行使价格,该头寸将显示最大利润。因此,短期铁蝴蝶等同于长期蝴蝶。图8-17展示了长期和短期铁蝴蝶的示例。

Another variation on a butterfly, known as a condor, can be constructed by splitting the inside exercise prices. Now the position consists of four options at consecutive exercise prices where the two outside options are purchased and the two inside options sold (a long condor), or the two inside options are purchased and the two outside options sold (a short condor). As with a butterfly, all options must be of the same type (all calls or all puts) and expire at the same time.

另一种变体称为秃鹫(condor),可以通过拆分内部行使价格来构建。此时,头寸由四个连续行使价格的期权组成,其中购买两个外部期权并卖出两个内部期权(长期秃鹫),或者购买两个内部期权并卖出两个外部期权(短期秃鹫)。与蝴蝶价差一样,所有期权必须是同一类型(全为看涨或全为看跌)并同时到期。

At expiration a condor will have its maximum value, equivalent to the amount between consecutive exercise prices, when the underlying contract is at or anywhere between the two inside exercise prices. It will be worthless whenever the underlying contract is outside the extreme exercise prices at expiration. Note that this is very similar to a butterfly, except that a condor has a maximum value over a wider range of underlying prices. A butterfly will achieve its maximum value at expiration at only one underlying price, when the underlying contract is right at the inside exercise price. For this reason a condor will usually have a higher value than a butterfly with approximately the same exercise prices. Examples of long and short condors are shown in Figure 8-18.

在到期时,当标的合约位于两个内部行使价格之间或正好处于其中一个内部行使价格时,秃鹫将具有最大价值,相当于连续行使价格之间的金额。当标的合约超出极限行使价格时,该头寸在到期时将变得毫无价值。注意,这与蝴蝶价差非常相似,区别在于秃鹫在更广泛的标的价格范围内具有最大价值。蝴蝶价差在到期时仅在一个标的价格下达到最大价值,即当标的合约正好处于内部行使价格时。因此,秃鹫通常比具有大致相同行使价格的蝴蝶价差具有更高的价值。图8-18展示了长期和短期秃鹫的示例。

SPREAD SENSITIVITIES

价差敏感性

Just as every individual option has a unique delta, gamma, theta, vega, and tho associated with it, every spread position has unique sensitivities. These numbers can help a trader determine beforehand how changing market conditions are likely to affect the spread. Before proceeding further the reader may want to review Figure 6-27, which summarizes the significance of the signs associated with the various option sensitivities.

每个单独的期权都有其独特的德尔塔(delta)、伽马(gamma)、西塔(theta)、维加(vega)等参数,每个价差头寸也有其独特的敏感性。这些数值可以帮助交易者提前判断市场条件变化对价差的影响。在进一步讨论之前,读者可以查看图6-27,以总结各种期权敏感性符号的意义。

A trader who initiates a volatility spread is concerned primarily with the magnitude of movement in the underlying contract and only secondarily with the direction of movement. Therefore all volatility spreads will be approximately delta neutral (the deltas will add up to approximately zero). It is true that some volatility spreads may prefer movement in one direction rather than the other, but the primary consideration is whether movement of any type will occur. If a trader has a large positive or negative delta, such that directional considerations become more important than volatility considerations, then the position can no longer be considered a volatility spread.

发起波动率价差的交易者主要关注标的合约的价格波动幅度,而次要关注波动的方向。因此,所有波动率价差基本上都是德尔塔中性的(德尔塔的总和接近零)。确实,有些波动率价差可能更倾向于某一方向的波动,但主要考虑因素是是否会发生任何类型的波动。如果交易者有较大的正或负德尔塔,使得方向考虑变得比波动考虑更重要,则该头寸不再被视为波动率价差。

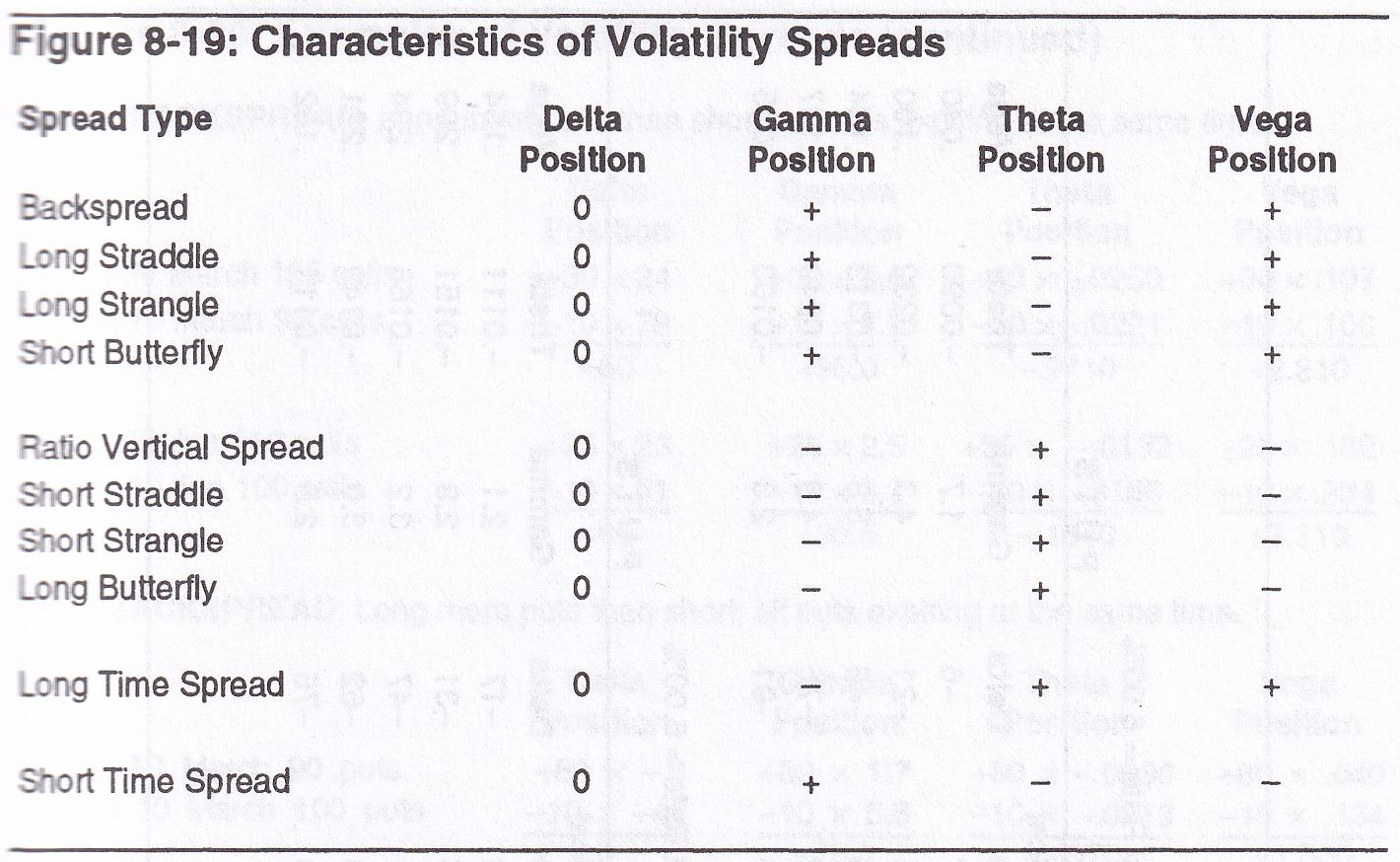

All spreads which are helped by movement in the underlying market have a positive gamma. These include backspreads, long straddles, long strangles, short butterflies, and short time spreads. All spreads which are hurt by movement in the underlying market will have a negative gamma. These include ratio vertical spreads, short straddles, short strangles, long butterflies, and long time spreads. A trader who has a positive gamma is sometimes said to be long premium and is hoping for a volatile market with large moves in the underlying contract. A trader who has a negative gamma is sometimes said to be short premium and is hoping for a quiet market with only small moves in the underlying market.

所有受标的市场波动影响的价差都有正伽马。这包括反向价差、长期跨式期权、长期跨价期权、短期蝴蝶价差和短期时间价差。所有因标的市场波动而受到损害的价差将具有负伽马。这包括比例垂直价差、短期跨式期权、短期跨价期权、长期蝴蝶价差和长期时间价差。拥有正伽马的交易者有时被称为“长期溢价”,希望市场波动剧烈,标的合约有较大价格变动。拥有负伽马的交易者有时被称为“短期溢价”,希望市场平静,仅有小幅波动。

Since the effect of market movement and the effect of time decay always work in opposite directions, any spread with a positive gamma will necessarily have a negative theta. Any spread with a negative gamma will necessarily have a positive theta. If market movement helps, the passage of time hurts. If market movement hurts, the passage of time helps. An option trader can't have it both ways.

由于市场波动和时间衰减的影响总是相反的,任何具有正伽马的价差必然会有负西塔。任何具有负伽马的价差必然会有正西塔。如果市场波动有利,则时间的推移是不利的;如果市场波动不利,则时间的推移是有利的。期权交易者不能同时获得这两者。

Spreads which are helped by a rise in volatility have a positive vega. These include backspreads, long straddles, long strangles, short butterflies, and long time spreads. Spreads which are helped by a decline in volatility have a negative vega. These include ratio vertical spreads, short straddles, short strangles, long butterflies, and short time spreads. In theory, the vega refers to the sensitivity of a theoretical value to a change in the volatility of the underlying contract over the life of the option. In practice, however, traders tend to associate the vega with the sensitivity of an option's price to a change in implied volatility. Spreads with a positive vega will be helped (hurt) by any increase (decrease) in implied volatility. Spreads with a negative vega will be helped (hurt) by any decrease (increase) in implied volatility.

受波动率上升影响的价差具有正维加。这包括反向价差、长期跨式期权、长期跨价期权、短期蝴蝶价差和长期时间价差。受波动率下降影响的价差具有负维加。这包括比例垂直价差、短期跨式期权、短期跨价期权、长期蝴蝶价差和短期时间价差。理论上,维加是指理论价值对标的合约波动率变化的敏感性。然而,在实际操作中,交易者往往将维加与期权价格对隐含波动率变化的敏感性联系起来。具有正维加的价差会因隐含波动率的任何增加而受益,反之亦然。具有负维加的价差会因隐含波动率的任何下降而受益,反之亦然。

The delta, gamma, theta, and vega associated with the primary types of volatility spreads are summarized in Figure 8-19. Since the delta of a volatility spread is assumed to be approximately zero, and since the theta is always of opposite sign to the gamma but of similar magnitude, we can place every volatility spread into one of four categories based on the sign of the gamma and vega associated with the spread:

| Category | Gamma | Vega |

|---|---|---|

| Backspread | Positive | Positive |

| Ratio Vertical Spread | Negative | Negative |

| Long Time Spread | Negative | Positive |

| Short Time Spread | Positive | Negative |

图8-19总结了主要波动率价差类型的德尔塔、伽马、西塔和维加。由于波动率价差的德尔塔被假定为接近零,且西塔总是与伽马符号相反但数值相似,我们可以根据价差的伽马和维加的符号将每个波动率价差归入四个类别之一:

| 类别 | Gamma | Vega |

|---|---|---|

| 反向价差 | 正 | 正 |

| 比例垂直价差 | 负 | 负 |

| 长期价差 | 负 | 正 |

| 短期价差 | 正 | 负 |

If a trader is approximately delta neutral—no matter how complex the position, even if it includes options of different types, at many different exercise prices, and with several different expiration dates—he can always place the position in one of these four general categories based on the gamma and vega of the position. The extent to which he is pursuing one of these strategies will depend on the magnitude of the gamma and vega. A trader with a gamma of -100 and vega of +200 would describe his position as a long time spread, but not nearly to the degree of a trader who has a gamma of -1500 and a vega of +3000.

如果交易者基本上是德尔塔中性的——无论头寸多复杂,即使包括不同类型的期权、不同的行权价和多个到期日——他总能根据头寸的伽马和维加将其归入这四个类别之一。他追求其中某一策略的程度将取决于伽马和维加的大小。例如,伽马为-100、维加为+200的交易者会将其头寸描述为长期时间价差,但程度上远不及伽马为-1500、维加为+3000的交易者。

Figure 8-20 is an evaluation table with the theoretical value, delta, gamma, theta, and vega of several different options. Following this table are examples of volatility spreads of the types discussed in this chapter, along with their total delta, gamma, theta, and vega. (Although the examples in Figure 8-20 are based on futures options, the spread characteristics are equally valid for stock options.) The reader will see that each spread does indeed have the positive or negative sensitivities summarized in Figure 8-19. Note also that a volatility spread need not be exactly delta neutral. (Indeed, as we saw in Chapter 6, no trader can say with any certainty whether he is delta neutral.) A practical guide is for the delta to be close enough to zero so that the volatility considerations are more important than the directional considerations.

图8-20是一个评估表,列出了几种不同期权的理论价值、德尔塔、伽马、西塔和维加。在此表之后是本章讨论的波动率价差示例,以及它们的总德尔塔、伽马、西塔和维加。(虽然图8-20中的例子基于期货期权,但价差特征同样适用于股票期权。)读者会看到每个价差确实具有图8-19中总结的正或负敏感性。需要注意的是,波动率价差不必完全德尔塔中性。(事实上,正如我们在第六章所看到的,没有交易者能确定自己是否德尔塔中性。)一个实用的标准是,德尔塔应足够接近零,以便波动率因素比方向因素更为重要。

Note that no price is given for any of the option contracts in Figure 8-20, and therefore no theoretical edge can be calculated for any of the spreads. The prices at which a spread is executed may be good or bad, resulting in a positive or negative theoretical edge. But once the spread has been established , the market conditions which will help or hurt the spread are determined by its type, not by the initial prices. Like all traders, option traders must not let their previous trading activity affect their current judgement. A trader's primary concern ought never be what happened yesterday, but what he can do today to make the most of the current situation, whether that means maximizing his potential profit or minimizing his potential loss.

注意,图8-20中没有给出任何期权合约的价格,因此无法为任何价差计算理论优势。价差执行时的价格可能好也可能坏,导致正或负的理论优势。但一旦建立了价差,帮助或损害该价差的市场条件由其类型决定,而不是由初始价格决定。像所有交易者一样,期权交易者必须避免让之前的交易活动影响当前判断。交易者的主要关注点永远不应是昨天发生的事情,而是他今天可以做些什么来充分利用当前情况,无论这意味着最大化潜在利润还是最小化潜在损失。

CHOOSING AN APPROPRIATE STRATEGY

选择合适的策略

With so many spreads available, how do we know which type of spread is best? First and foremost we will want to choose spreads which have a positive theoretical edge to ensure that if we are right about market conditions we can be confident of showing a profit. Ideally, we would like to construct a spread by purchasing options which are underpriced and selling options which are overpriced. If we can do this the resulting spread, whatever its type, will always have a positive theoretical edge.

在众多可用的价差中,如何选择最佳的类型?首先,我们希望选择具有正理论优势的价差,以确保在我们对市场条件的判断正确时能够获利。理想情况下,我们希望通过购买低估的期权并出售高估的期权来构建价差。如果能够做到这一点,不论价差类型如何,结果总会具有正理论优势。

More often, however, our opinion about volatility will result in all options appearing either underpriced or overpriced. When this happens, it will be impossible to both buy underpriced and sell overpriced options. Such a market can be easily identified by comparing our volatility estimate to the implied volatility in the option marketplace. If implied volatility is generally lower than our volatility estimate, all options will appear underpriced. If implied volatility is generally higher than our estimate, all options will appear overpriced

然而,更多情况下,我们对波动率的看法会导致所有期权都显得低估或高估。当这种情况发生时,就不可能同时购买低估的期权和出售高估的期权。可以通过将我们的波动率估算与期权市场中的隐含波动率进行比较来轻松识别此类市场。如果隐含波动率通常低于我们的波动率估算,则所有期权都将显得低估;如果隐含波动率通常高于我们的估算,则所有期权都将显得高估。

If options generally appear underpriced (low implied volatility), look for spreads with a positive vega. This includes strategies in the backspread or long time spread category. If options generally appear overpriced (high implied volatility), look for spreads with a negative vega. This includes strategies in the ratio vertical or short time spread category.

如果期权普遍显得低估(隐含波动率低),可以寻找具有正维加的价差,这包括反向价差或长期时间价差策略。如果期权普遍显得高估(隐含波动率高),则应寻找具有负维加的价差,这包括比例垂直价差或短期时间价差策略。

It may seem at first glance that if one encounters a market where all options are either underpriced or overpriced, the sensible strategies are either long straddles and strangles, or short straddles and strangles. Such strategies will enable a trader to take a position with a positive theoretical edge on both sides of the spread. Straddles and strangles are certainly possible strategies when all options are too cheap or too expen-sive. We will see in Chapter 9 that straddles and strangles, while often having a large, positive theoretical edge, can also be among the riskiest of all strategies. For this reason, a trader will often want to consider other spreads in the backspread or ratio vertical spread category, even if such spreads entail buying some overvalued options or selling some underpriced options.

乍一看,如果遇到所有期权都显得低估或高估的市场,合理的策略似乎是进行多头平价期权和波动期权,或者做空平价期权和波动期权。这些策略将使交易者在价差的两侧都能获得正理论优势。当所有期权都太便宜或太贵时,平价期权和波动期权确实是可行的策略。我们将在第九章看到,尽管平价期权和波动期权通常具有较大的正理论优势,但它们也可能是所有策略中风险最高的。因此,交易者通常会考虑其他类型的价差,比如反向价差或比例垂直价差,即使这些价差可能需要购买一些高估的期权或出售一些低估的期权。

The theoretical values and deltas in Figure 8-20 have been reproduced in Figures 8-21 and 8-22, but now prices have been included which reflect implied volatilities different from the volatility input of 20%. The prices in Figure 8-21 reflect an implied volatility of 17%. In this case the reader will find that only those spreads with a positive vega will have a positive theoretical value:

call and put backspreads

long straddles and strangles

short butterflies

long time spreads

图8-20中的理论值和德尔塔在图8-21和图8-22中重复出现,但现在包含了反映不同于20%波动率输入的隐含波动率的价格。图8-21中的价格反映了17%的隐含波动率。在这种情况下,读者会发现只有那些具有正维加的价差才会有正理论值:

看涨和看跌反向价差

多头平价期权和波动期权

空头蝴蝶价差

长期时间价差

The prices in Figures 8-22 reflect an implied volatility of 23%. Now the reader will find that only those spreads with a negative vega will have a positive theoretical value:

call and put ratio vertical spreads

short straddles and strangles

long butterflies

short time spreads

图8-22中的价格反映了23%的隐含波动率。现在,读者会发现只有那些具有负维加的价差才会有正理论值:

看涨和看跌比例垂直价差

空头平价期权和波动期权

多头蝴蝶价差

短期时间价差

An important assumption in most theoretical pricing models is that volatility is constant over the life of an option. The volatility input into the model is assumed to be the one volatility which best describes price fluctuations in the underlying instrument over the life of the option. When all options expire at the same time, it is this one volatility which will, in theory, determine the desirability of a spread. In real life, however, a trader may believe that volatility is likely to rise or fall over some period of time. Very often implied volatility will also rise or fall. Since time spreads are particularly sensitive to changes in implied volatility, whether volatility is rising or falling can affect the desirability of time spreads. Consequently, we can add this corollary to our spread guidelines: Long time spreads are likely to be profitable when implied volatility is low but is expected to rise; short time spreads are likely to be profitable when implied volatility is high but is expected to fall.

大多数理论定价模型的重要假设是波动率在期权生命周期内是恒定的。模型中的波动率输入被认为是最能描述标的资产价格波动的波动率。当所有期权同时到期时,这一波动率理论上将决定价差的可取性。然而,在实际操作中,交易者可能认为波动率在某段时间内会有升降变化。隐含波动率往往也会随之波动。由于时间价差对隐含波动率的变化特别敏感,波动率的升降会影响时间价差的可取性。因此,我们可以将以下附加规则纳入价差指南:当隐含波动率较低且预计会上升时,多头时间价差可能会盈利;当隐含波动率较高且预计会下降时,空头时间价差可能会盈利。

These are only general guidelines, and an experienced trader may decide to violate them if he has reason to believe that the implied volatility will not correlate with the volatility of the underlying contract. A long time spread might still be desirable in a high implied volatility market, but the trader must make a prediction of how implied volatility might change under certain conditions. If the market were to stagnate, with no movement in the underlying contract, but the trader felt that implied volatility would remain high, a long time spread would be a sensible strategy. The short-term option would decay, while the long-term option would retain its value. In the same way, a short time spread might still be desirable in a low implied volatility market if the trader felt that the underlying instrument were likely to make a large move with no commensurate increase in implied volatility.

这些只是一般指导原则,经验丰富的交易者可能会根据隐含波动率与标的合约波动率不相关的原因决定违反这些原则。在高隐含波动率市场中,多头时间价差仍然可能是可取的,但交易者必须预测在某些条件下隐含波动率的变化。如果市场停滞,标的合约没有波动,而交易者认为隐含波动率将保持高位,那么多头时间价差就是一种合理的策略。短期期权会贬值,而长期期权则会保值。同样地,如果交易者认为标的资产可能会有较大波动,但隐含波动率没有相应增加,空头时间价差在低隐含波动率市场中也可能是可取的。

ADJUSTMENTS

调整

A volatility spread may initially be delta neutral, but the delta of the position is likely to change as the price of the underlying contract rises or falls. Moreover, changes in volatility and time to expiration can also affect the delta of spread. A spread which is delta neutral today may not be delta neutral tomorrow, even if all other conditions remain the same. The optimum use of a theoretical pricing model requires a trader to continuously maintain a delta neutral position throughout the life of the spread. Continuous adjustments are impossible in real life, so a trader ought to give some thought to when he will adjust a position. Essentially, we can consider three possibilities:

波动率价差最初可能是delta中性的,但随着标的合约价格的涨跌,头寸的delta可能会变化。此外,波动率和到期时间的变化也会影响价差的delta。今天是delta中性的价差,明天可能就不再中性,即使其他条件保持不变。理论定价模型的最佳使用要求交易者在价差的生命周期内持续维持delta中性头寸。现实中无法做到持续调整,因此交易者需要考虑何时调整头寸。基本上,我们可以考虑三种可能性:

1. Adjust at regular intervals-In theory, the adjustment process is assumed to be continuous because volatility is assumed to be a continuous measure of the speed of the market. In practice, however, volatility is measured over regular time intervals, so a reasonable approach is to adjust a position at similar regular intervals.

1. 定期调整——理论上,调整过程被假设为连续进行,因为波动率被视为市场速度的连续指标。然而,实际操作中波动率是通过定期时间间隔来衡量的,因此合理的做法是在类似的时间间隔内调整头寸。

If a trader's volatility estimate is based on daily price changes, the trader might adjust daily. If the estimate is based on weekly price changes, he might adjust weekly. This is a trader's best attempt to emulate the assumptions built into the theoretical pricing model.

如果交易者的波动率估算是基于每日价格变化,交易者可以每天调整。如果估算是基于每周价格变化,则可以每周调整。这是交易者尽量模拟理论定价模型中假设的最佳尝试。

2. Adjust when the position becomes a predetermined number of deltas long or short—Very few traders insist on being delta neutral all the time. Most traders realize that this is not a realistic approach, both because a continuous adjustment process is physically impossible, and because no one can be certain that all the assumptions and inputs in a theoretical pricing model, from which the delta is calculated, are correct. Even if one could be certain that all delta calculations were accurate, a trader might still be willing to take on some directional risk. But a trader ought to know just how much directional risk he is willing to accept. If he wants to pursue delta neutral strategies, but believes that he can comfortably live with a position which is up to 500 deltas long or short, then he can adjust the position any time his delta position reaches this limit. Unlike the trader who adjusts at regular intervals, a trader who adjusts based on a fixed number of deltas cannot be sure how often he will need to adjust his position. In some cases he may have to adjust very frequently; in other cases he may go for long periods of time without adjusting.

2. 当头寸变成预定数量的delta多头或空头时进行调整——很少有交易者会要求自己始终保持delta中性。大多数交易者意识到,这种做法不切实际,因为持续调整过程在物理上不可能,而且没有人能确定理论定价模型中的所有假设和输入(从中计算delta)都是正确的。即使能确定所有delta计算都是准确的,交易者仍可能愿意承担一些方向风险。但交易者应该知道自己愿意接受多少方向风险。如果他想追求delta中性策略,但认为可以接受最多500个delta的头寸,那么他可以在delta头寸达到这一限制时随时调整。与定期调整的交易者不同,基于固定数量delta进行调整的交易者无法确定需要多频繁调整头寸。在某些情况下,他可能需要非常频繁地调整,而在其他情况下,可能会很长时间不进行调整。

The number of deltas long or short a trader chooses for his adjustment points depends on the size of his positions and his capitalization. A small, independent trader may find that he is uncomfortable with a position which is even 200 deltas long or short, while a large trading firm may consider a position which is several thousand deltas long or short as being approximately delta neutral.

交易者选择的用于调整点的delta数量取决于其头寸规模和资本情况。小型独立交易者可能发现即使200个delta的头寸也让他感到不安,而大型交易公司可能将数千个delta的头寸视为近似delta中性。